It's the supply, stupid

It's the supply, stupid

Nine misconceptions about why housing is so expensive

This week the British government released a white paper on housing and the land-use planning system that could actually be pretty good, if it makes it into law. Its basic aim is to move England to a zoning-based system where local councils set out rules about what can be built where, but don’t take an active role in approving or rejecting individual applications for development. Rules over discretion.

Many objections to this approach are based on (what I see as) misconceptions about how the housing market works. These are sometimes presented as the “real” reason that housing is too expensive, in contrast with unsophisticated supply-focused explanations. In this issue of Consumer Surplus I try to explain why many of these are conceptually and/or factually flawed, and it really is regulatory constraints on supply that are the problem.

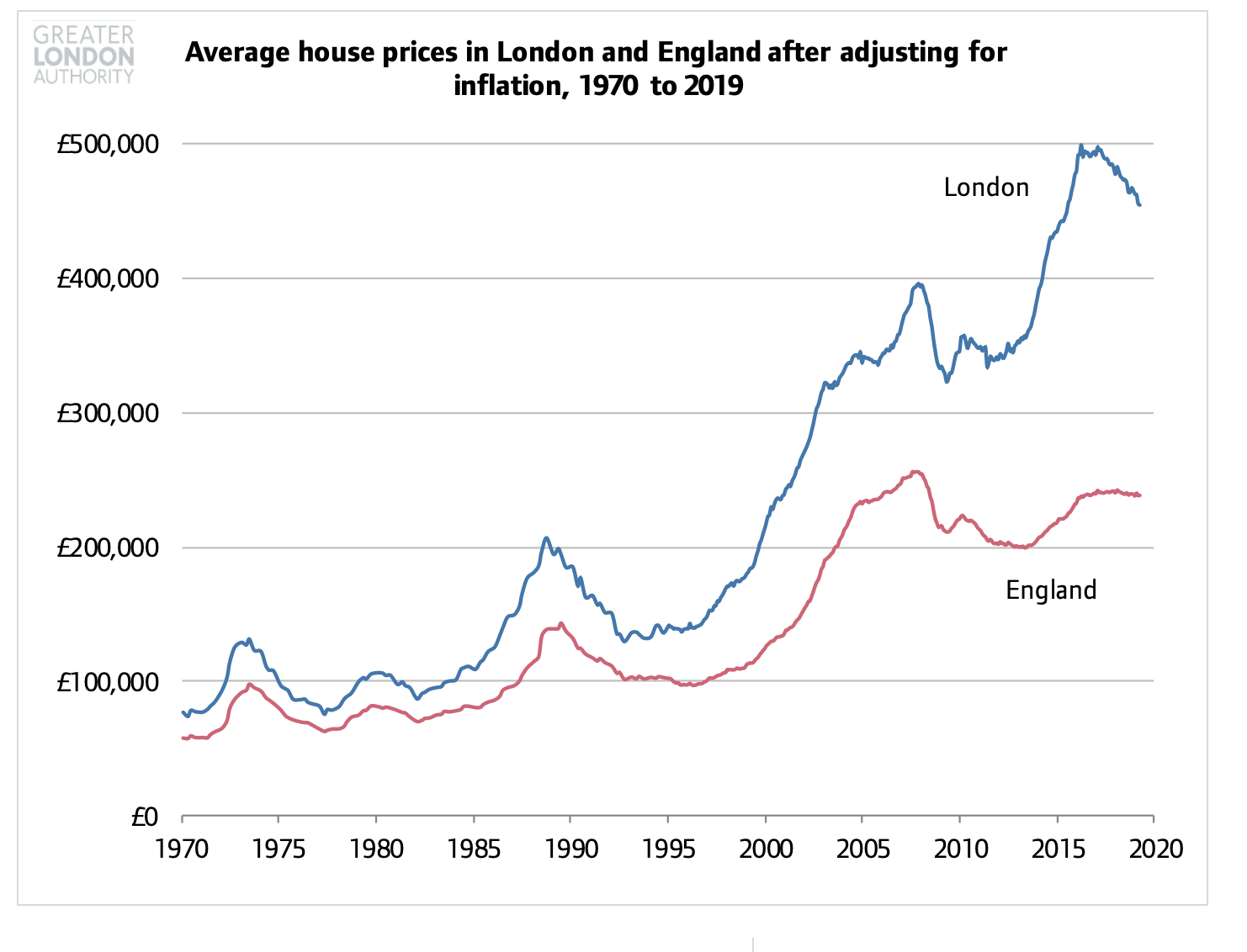

“House prices are high because of interest rates, not a lack of supply.” This is true insofar as falling interest rates do raise house prices, by making the cost of mortgage borrowing lower and making rental yields relatively more attractive. But the effect works with constrained supply as two blades of a scissors: housing is an investment good whose price is affected by interest rates, but only when its supply is constrained.

Falling interest rates do not increase the price of other durable goods like airplanes or ships, or of housing in places where there is not a supply constraint, like in the North of England or Houston (which has a liberalised planning system). If interest rates were the only factor, we would expect to see houses everywhere rise and fall in line with them. But they only do so in places where supply, significantly constrained by planning laws, cannot meet the demand.

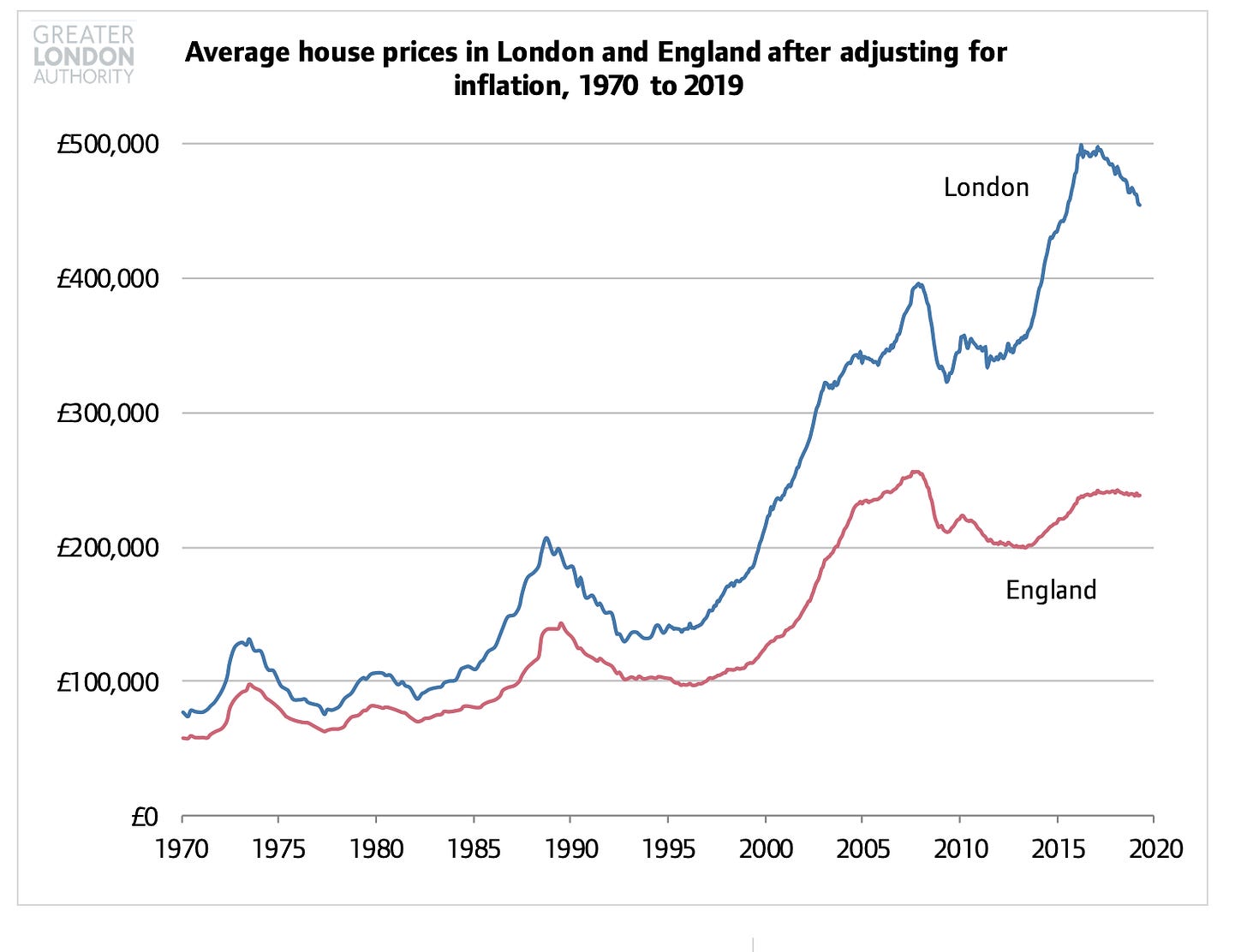

In this chart, if interest rates were the only factor affecting prices, we should not expect to see a big divergence between prices in London and the rest of the UK. Instead, we see that from the early 2000s prices rise far more in London than England as a whole, and spike especially rapidly in the first half of the 2010s, whereas growth is much more muted in the rest of the country.

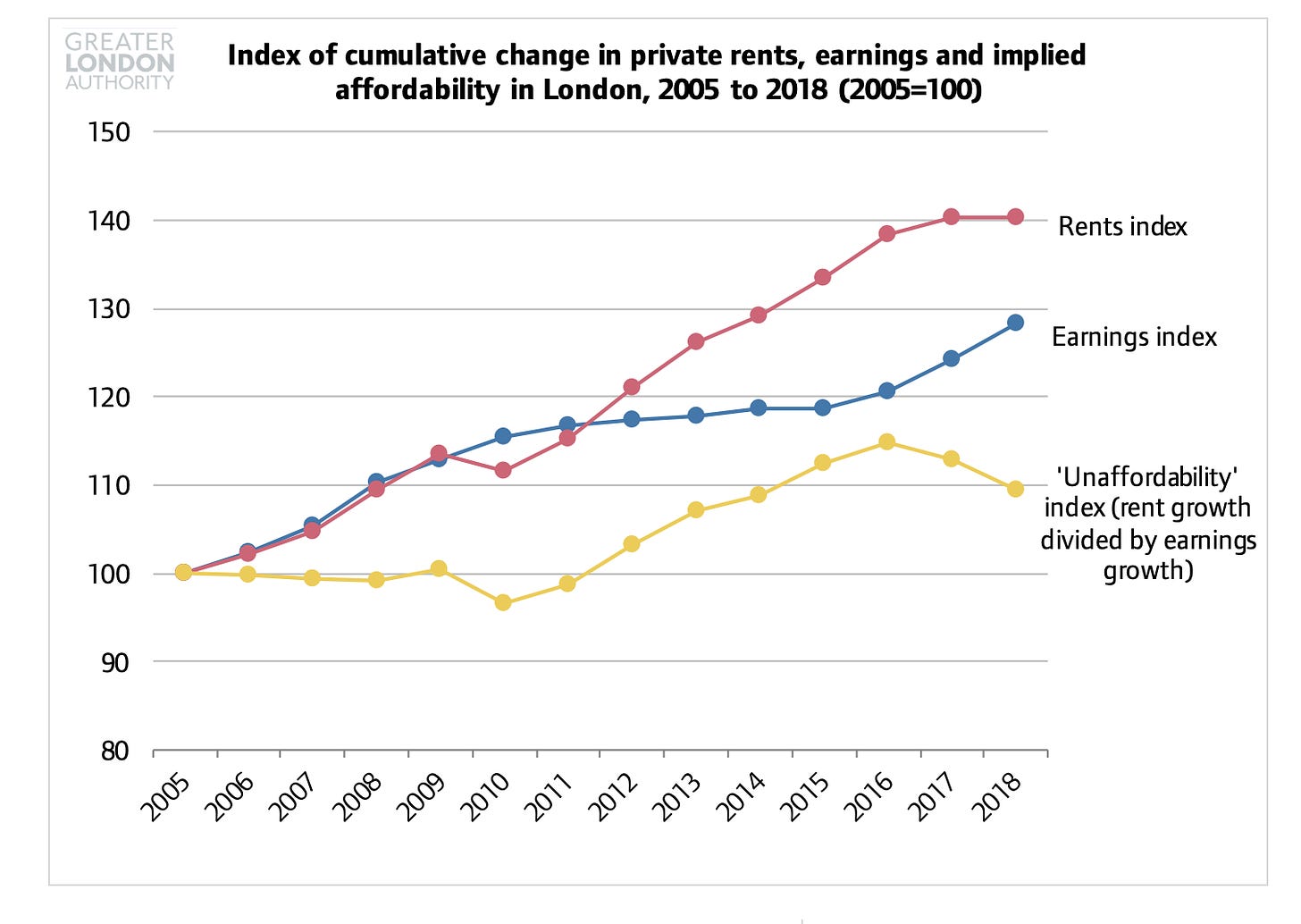

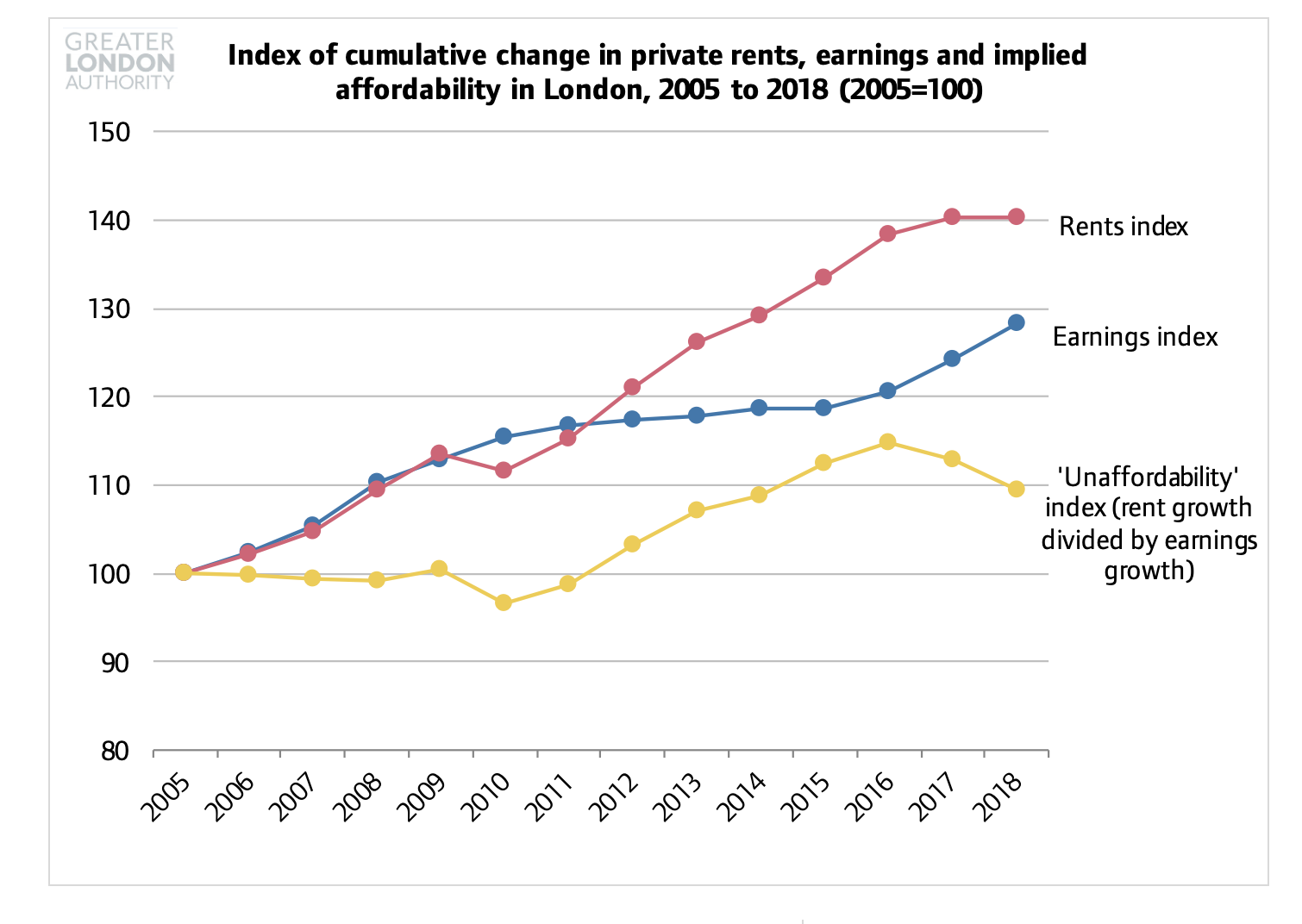

“Rents haven’t been rising as a share of income, so there is no shortage.” This misconception has two big errors. The first is that it looks at the national, aggregate figures, when the claim is that there is a shortage of housing in specific parts of the UK like London and Oxford. If you look at those places, rents have been rising well above earnings.

The second error is more important: rents have in fact been rising on aggregate, just not as a share of people’s income across the UK as a whole. In other words, as we get richer as a society, the share we are spending on rent remains the same, without a quality improvement. This is a sign of constrained supply (a fixed amount of supply being bid up and up as we get richer). And it is a disaster – it means that a lot of income growth people experience does not actually benefit them, but goes into rents instead. Suppose everything we spent money on changed in the same way, rising in real-terms as we got richer – groceries, electricity, clothes – without getting any better in quality. Economic growth would be meaningless, because any overall income growth we experienced would simply be eaten up by these rising costs.

“The elasticity of house prices to new supply is low, so building more houses won’t do much to lower prices.” If this was true, it would be great news. It would mean that building more houses would make us even richer than we thought – if we could build millions more, and prices still didn’t fall by very much, then we’d have basically invented a free money machine. Unfortunately, although we can create a lot of extra wealth and value by allowing more houses to be built, this misconception gets price elasticity the wrong way around.

A low price elasticity – prices not falling by much when supply rises – tells us the exact opposite to there being little unmet demand for more housing. It tells us that there is so much unmet demand, even if we built tens of thousands of new houses, people would still want them so much that prices would stay high. On its own, that would be fine – better to meet demand and allow someone to buy a house they want, even if they pay a high price for it. But combined with the “wedge” between the current market price and the cost of new building, price elasticity can tell us how many new houses we would need to build to get market prices down to roughly match build costs – in other words, eliminating the artificial scarcity that currently accounts for more than half the cost of houses in the South East of England. If it is low, and adding lots more houses would still not make much of a dent in house prices overall, it suggests that the shortage is very significant.

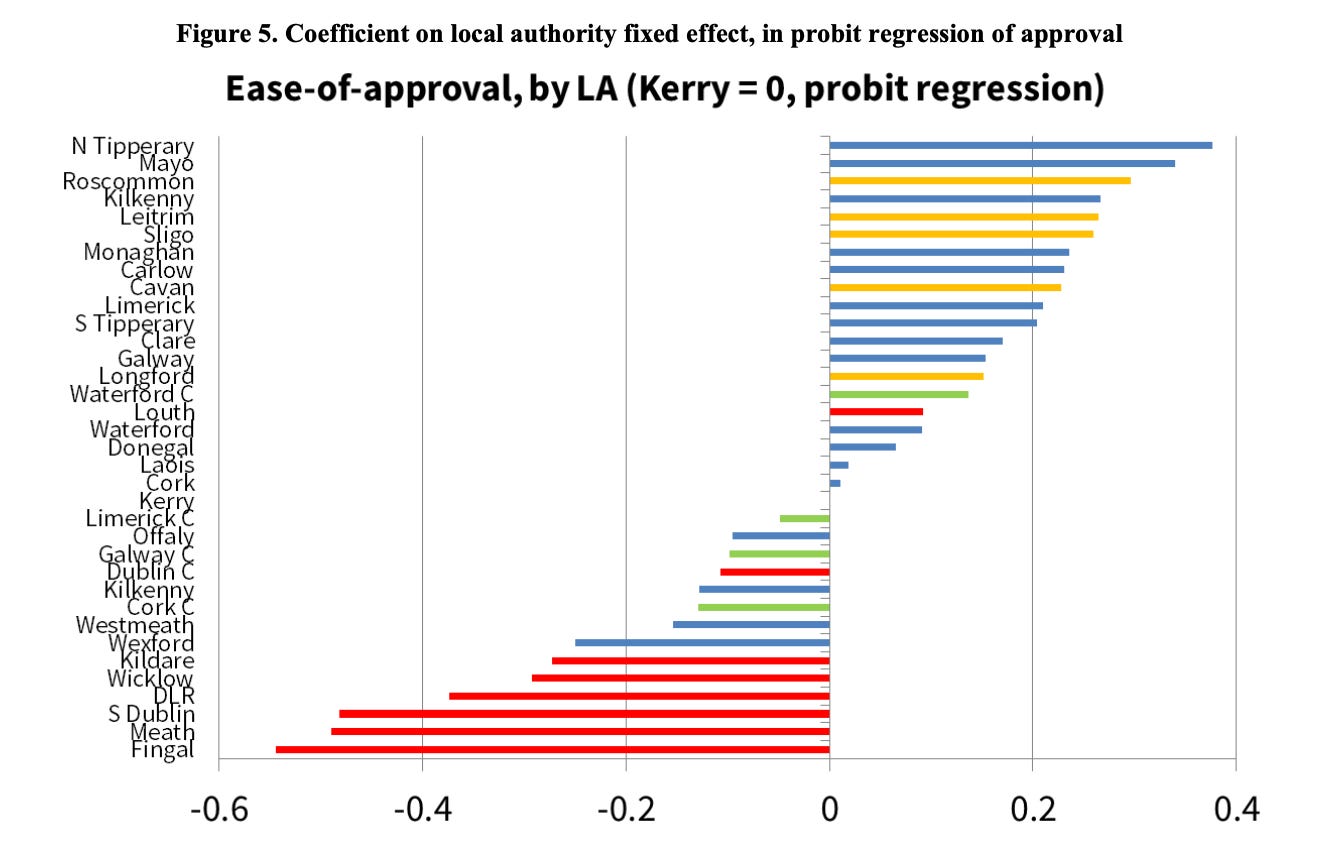

Imagine a similar argument being made during a famine where the price of food was very high: if an additional food shipment did not make a big dent in overall prices, would we conclude that the solution wasn’t more food?“Nine out of ten planning applications are granted, so the problem isn’t the planning system.” This is wrong because you don’t apply for planning permission if you don’t expect to get it. I’d love to build a block of flats on my Zone 2 house, but I’m not even going to bother asking because I know I won’t be allowed. If we applied for permission for everything we would like to build, we would get something like a 99% rejection rate, not 90% acceptance.

“Land banking is the cause of housing shortages.” Property developers queue up a supply of land with planning permission because they need to ensure that they have somewhere to use their equipment and employees in the coming year. It appears, at first glance, like they are hoarding land. But this queuing is only necessary because the supply of land you can build on is so scarce and uncertain.

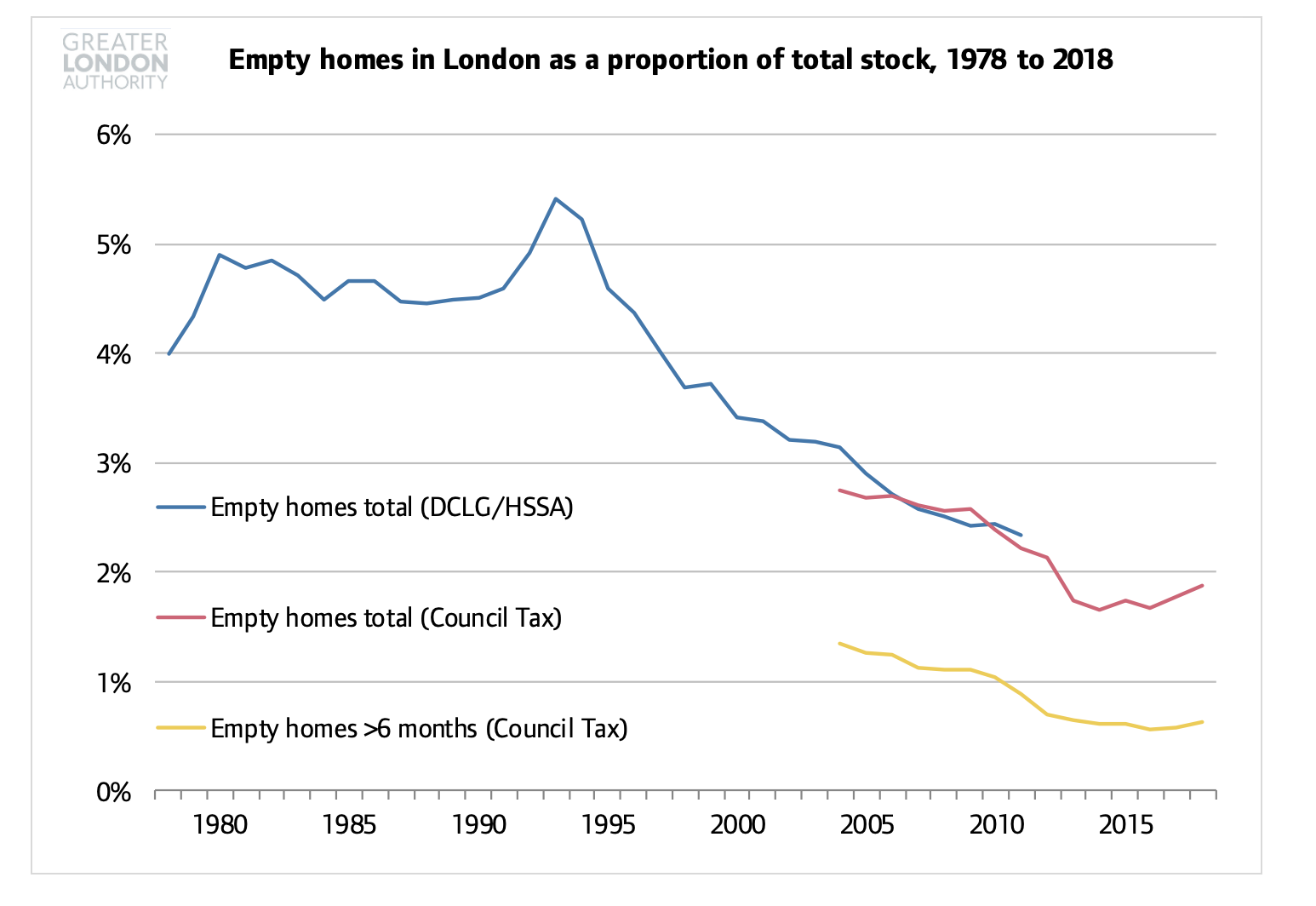

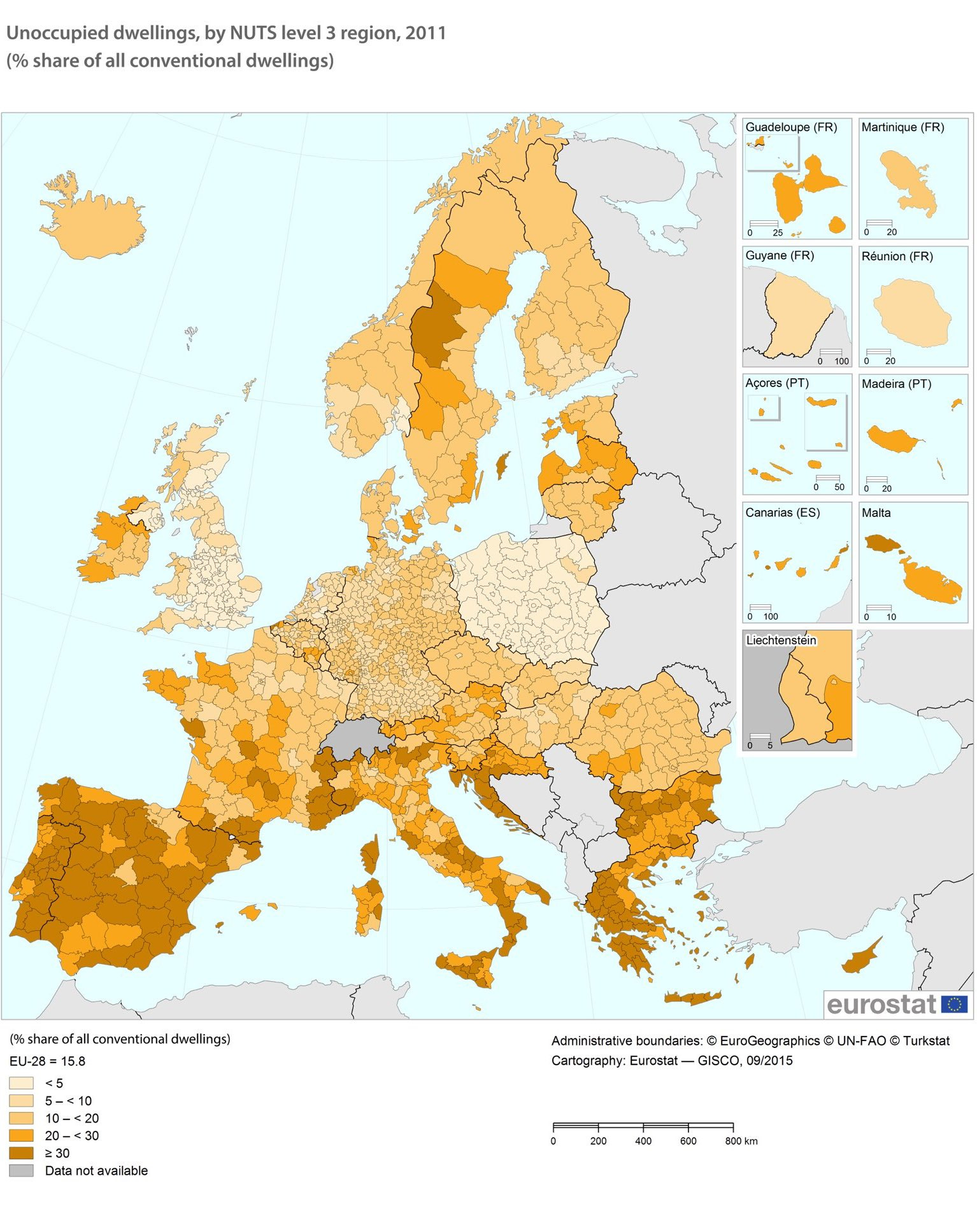

Twitter’s @jprwg made a good analogy: “Rather than 'land banking', call it 'land buffering'. Just as with video streaming, if you have a fast & reliable connection - you can easily get permission to build - you don't need to buffer. If your connection is slow & unreliable, you need to store up a reserve.” Land banking is a symptom of shortages. Not a cause.“Empty properties make the housing shortage worse.” Some number of empty properties is normal in a housing market where there is churn between people moving from one place to another, just as you will always have some unemployment as people move between jobs, although empty properties are sometimes a sign of an inefficient market.

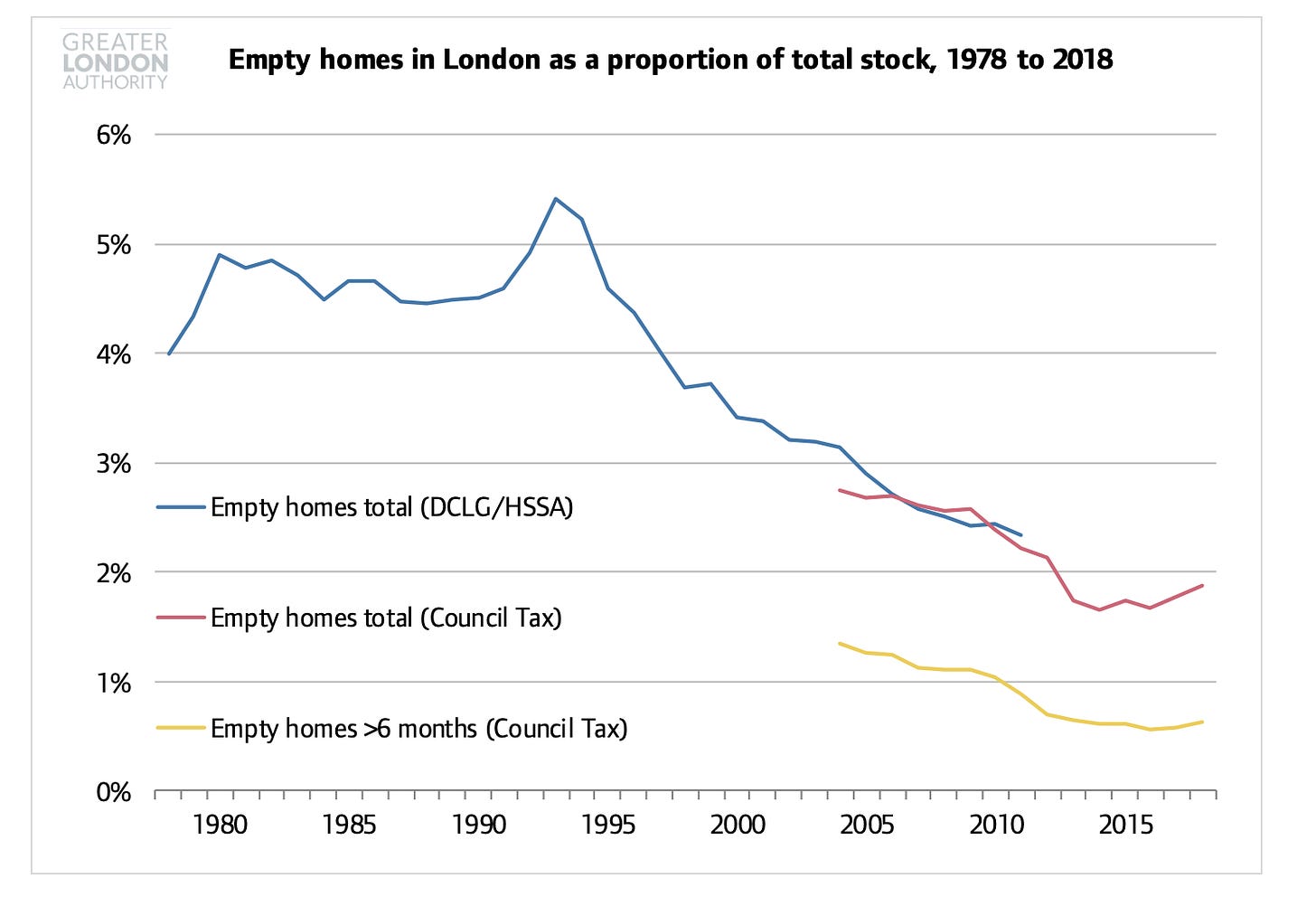

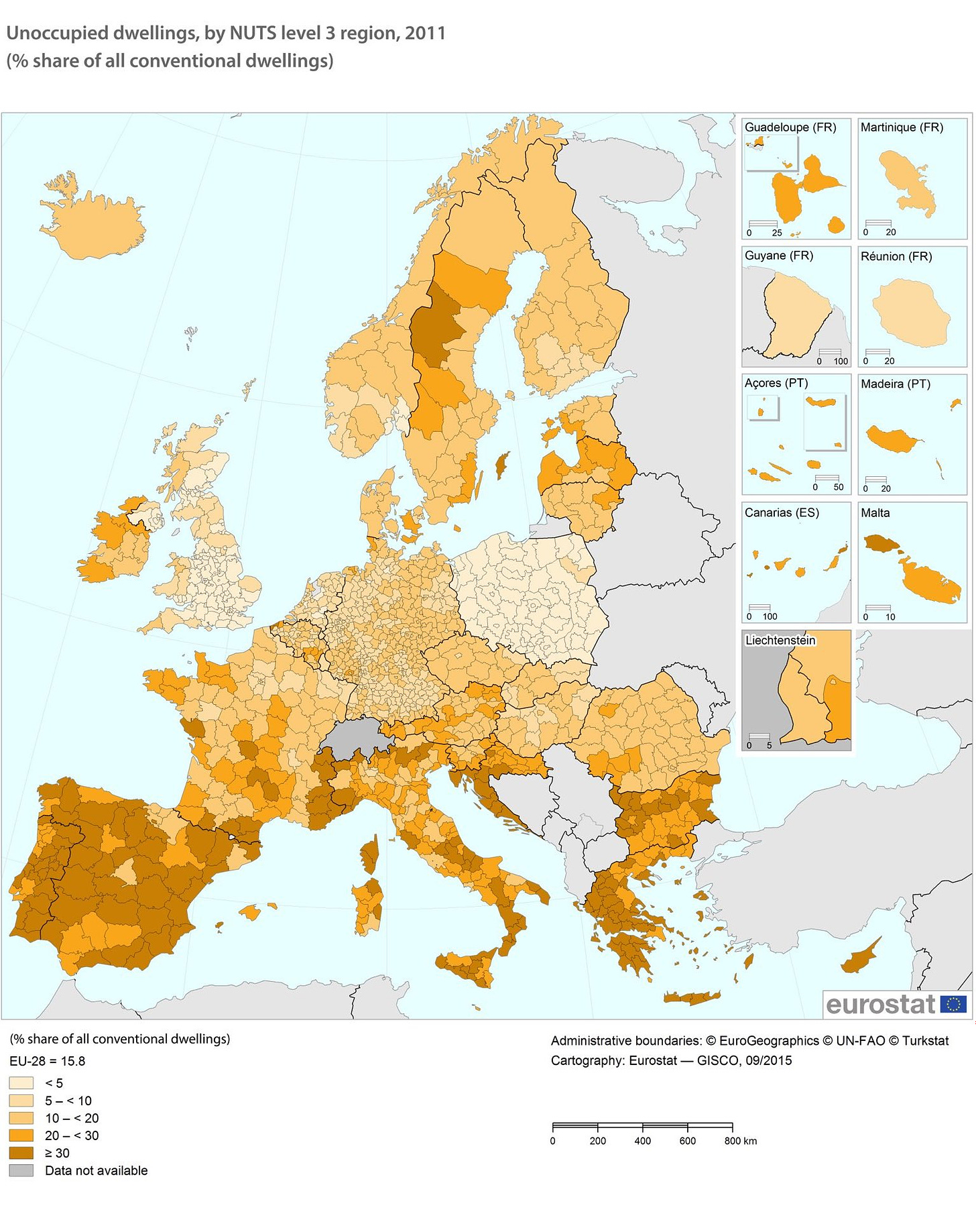

There are fewer properties being left empty in London today than at any point since the Second World War, and the UK as a whole is well below the rest of Europe in terms of unoccupied dwellings as a share of the total – virtually all regions with fewer than 5% of their dwellings unoccupied were either in Poland or the UK.

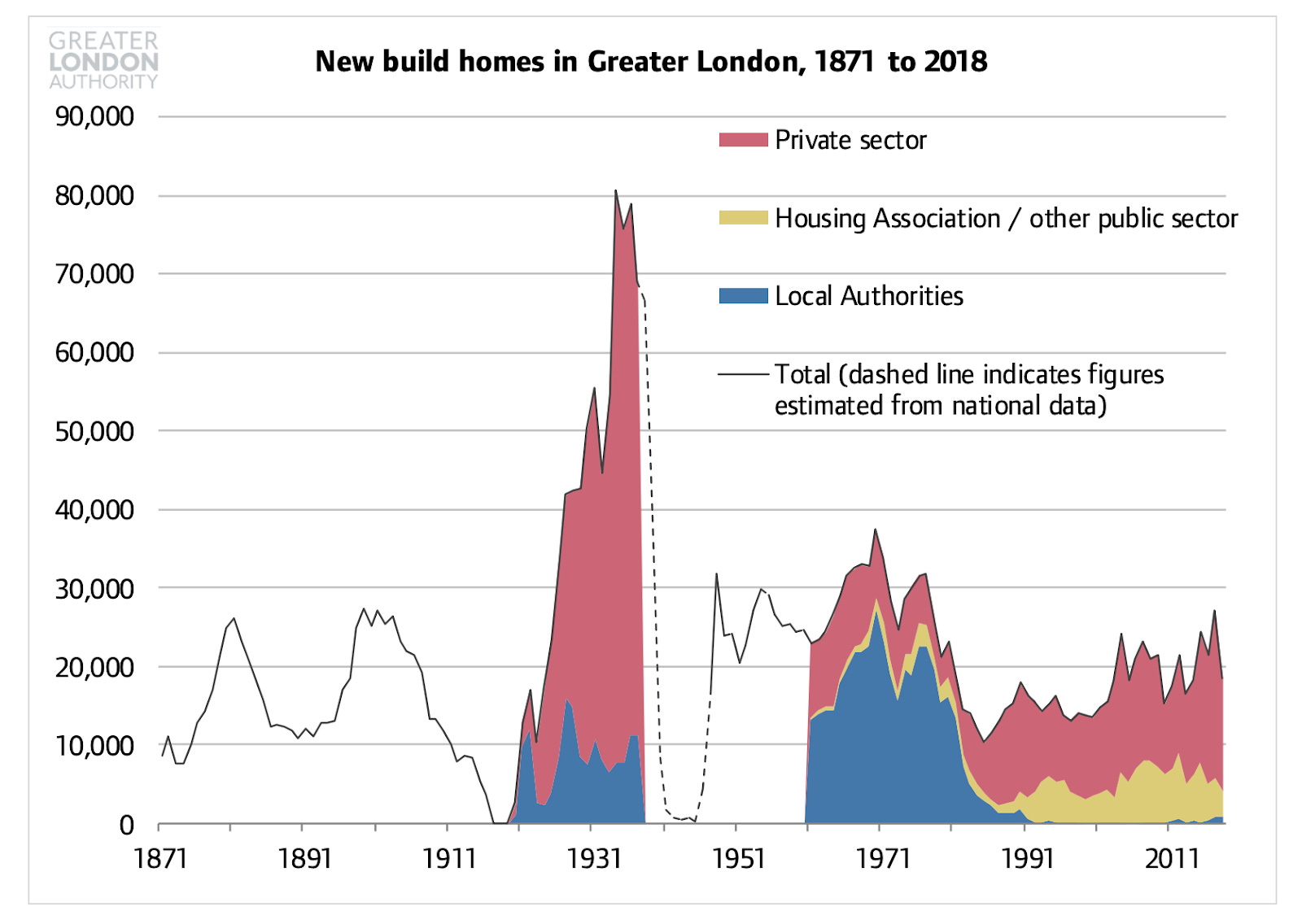

“The private sector cannot build enough houses to meet demand.” The evidence for this is extremely weak – it is based on the claim that the private sector did not increase construction to offset the reduced amount of council housing following the 1980s. But this has been a period where planning has severely constrained private building (that’s the whole problem!).

In the 1930s, there was a housebuilding boom that was almost entirely done by the private-sector. According to the economic historian Nicholas Crafts, “The number of houses built by the private sector rose from 133,000 in 1931-32 to 293,000 in 1934-35 and 279,000 in 1935-36”, and were responsible for one third of the increase in GDP from 1932 to 1934. If you actually let the private sector build, it will.

“It is impossible to make housing “affordable” without council housing / affordable housing.” There’s an alternative framing of this myth, which is that there is too much “luxury housing” being built. But this ignores how supply works. Think of the housing market like an ice cube tray: people at the top of the market will try to buy up as much of the best housing they can. Once that’s all taken, they’ll move to fill up the next-best housing “section”, pushing prices up for people there, who move down to the next section, pushing up prices there, and so on.

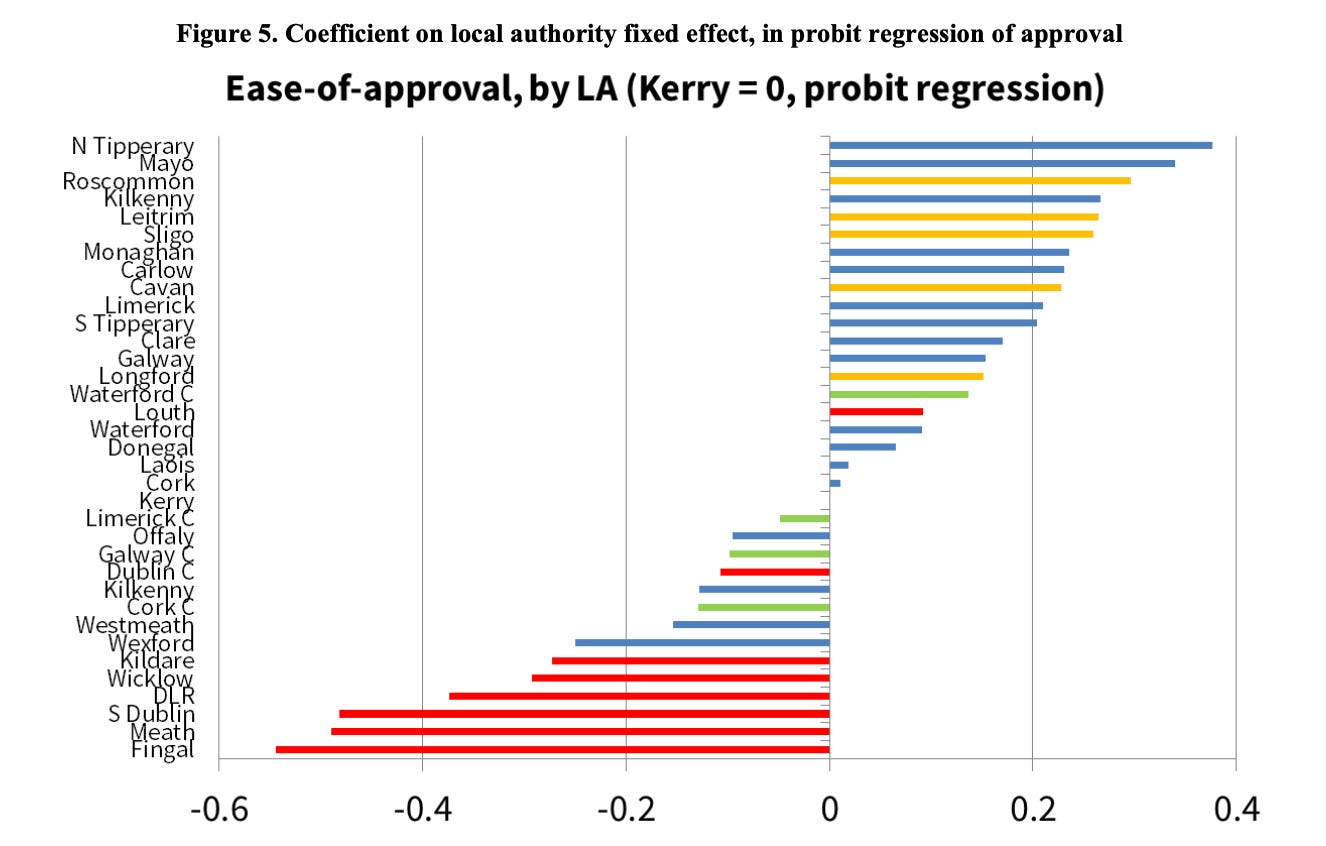

So building at the top of the market can relieve pressure on the bottom of the market. The more we build nicer things, the more those nice things become the norm - and fall in price. The alternative would be to have a housing stock that was falling in quality over time, as the existing stock degraded through wear and tear and we insisted on new construction being below-average to be “affordable”.“We risk speculative development after building booms which leaves us with ghost towns.” Ireland’s notorious “ghost estates” were not created by planning liberalisation. Research by Trinity College Dublin’s Ronan Lyons concludes that “credit, and credit alone, was to blame for the severity of Ireland’s housing market bubble” – and Ireland’s planning system made this worse by preventing construction in Dublin and other urban areas.

This chart shows how the planning system directed new construction to rural areas (yellow) instead of Dublin (red). Ireland’s “ghost estates” were a consequence of its planning system, making a property boom worse by driving construction to places where it was needed least.

Most of the charts in this issue come from the GLA’s incredible Housing In London report.